Buying a home in the United States almost always involves a mortgage. Most buyers do not pay cash. They borrow money from a lender and repay it over time with interest. That process sounds simple, but the details can be confusing at first.

Homeownership remains a major financial step for American families. Data from the U.S. Census Bureau shows that the national homeownership rate has stayed above 65% in recent years. That means millions of buyers go through the mortgage process each year.

Mortgage rules also change over time. Federal consumer protection standards under the Truth in Lending Act and the Real Estate Settlement Procedures Act require lenders to provide documents, including the Loan Estimate and the Closing Disclosure. The Consumer Financial Protection Bureau explains these forms in detail and updates guidance when regulations shift. Staying informed is important because loan limits, insurance premiums, and qualification standards can change from year to year.

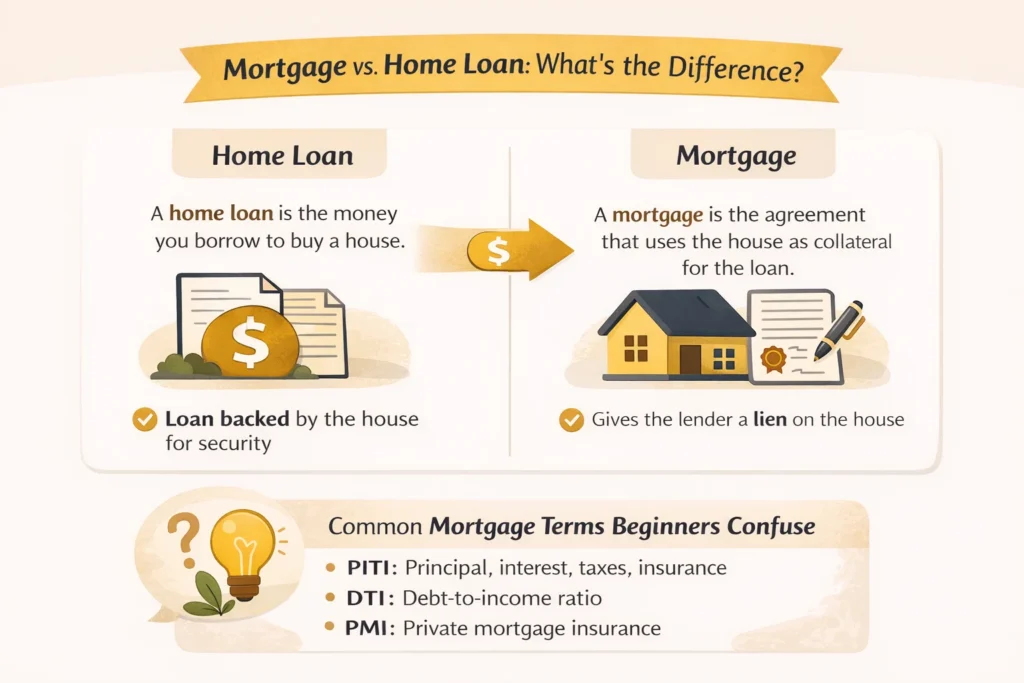

Mortgage vs. Home Loan: What Is the Difference?

People often use the terms “home loan” and “mortgage” as if they mean the same thing. They are closely connected but not identical.

- A home loan refers to the money you borrow.

- A mortgage refers to the legal agreement that secures a loan with your property.

Understanding this distinction helps you grasp how lenders protect their money and what rights you have as a borrower.

What is a home loan?

A home loan is a sum of money that a bank, credit union, or mortgage lender gives you to buy a house. You agree to repay that money over a set number of years, usually 15 or 30 years, along with interest.

Example:

You want to buy a home priced at 400,000 dollars. You made a 40,000-dollar down payment. A lender provides the remaining 360,000 dollars as a home loan. You then repay that 360,000 dollars over time, plus interest, through monthly payments.

That borrowed amount is your home loan.

In the United States, most home loans fall into two broad categories:

- Conventional loans

- Government-backed loans such as FHA, VA, or USDA loans

Each type has different credit, income, and down payment requirements. We will cover those in detail in later sections.

What is a mortgage?

A mortgage is a legal agreement that ties your home to the loan.

When you sign closing documents, you agree that the property serves as collateral for the loan. Collateral means the lender has a legal claim to the home if you stop making payments.

If a borrower fails to make payments for an extended period, the lender may initiate a legal process known as foreclosure. Foreclosure allows the lender to take possession of the property and sell it to recover the remaining balance of the loan.

State laws govern how foreclosure works, and timelines vary depending on whether the state uses judicial or non-judicial foreclosure procedures.

The key idea is simple.

- The home loan is the money.

- The mortgage is the legal security that protects the lender.

You cannot obtain a typical U.S. home loan without a mortgage agreement.

What does a mortgage payment include?

Most people focus only on the loan amount and interest rate. Your monthly mortgage payment usually includes more than that.

Lenders often describe the full monthly payment using the term PITI:

- Principal – The portion of your payment that reduces the loan balance.

- Interest – The cost you pay to borrow the money. Your interest rate determines how much this costs over time.

- Taxes – Property taxes assessed by your local government. Many lenders collect these monthly and hold them in an escrow account.

- Insurance – Homeowners insurance protects against damage and liability. Some borrowers also pay mortgage insurance if their down payment is small.

Example:

You take out a 360,000-dollar loan at a fixed interest rate. Your principal and interest payments might total $2,200 per month. Property taxes add 400 dollars. Homeowners insurance adds 150 dollars. Your total monthly payment becomes 2,750 dollars.

Buyers often underestimate this full payment. A lender qualifies you based on the complete monthly obligation, not just principal and interest.

Common mortgage terms beginners confuse

Mortgage language can feel overwhelming at first. Let’s clarify a few terms that create the most confusion.

Interest rate vs APR

The interest rate shows the percentage charged on the loan balance. It determines your principal and interest payment.

APR stands for annual percentage rate. APR includes the interest rate plus certain lender fees, rolled into an annual cost. Federal law requires lenders to disclose APR under the Truth in Lending Act. APR helps you compare loan offers more accurately because it reflects the broader cost of borrowing.

A loan with a lower interest rate can still have a higher APR if fees are higher.

Escrow

An escrow account is a separate account your lender uses to collect property taxes and insurance. You pay a portion each month. The lender then pays your tax bill and insurance premium on your behalf when they come due.

Escrow protects both you and the lender. Taxes and insurance stay current, which protects the property securing the loan.

Points

Mortgage points are upfront fees you can pay to lower your interest rate. One point typically equals 1% of the loan amount.

On a $360,000 loan, one point costs $3,600. In exchange, the lender reduces your interest rate by a set amount. Points can make sense if you plan to keep the home for many years. They make less sense if you expect to sell or refinance soon.

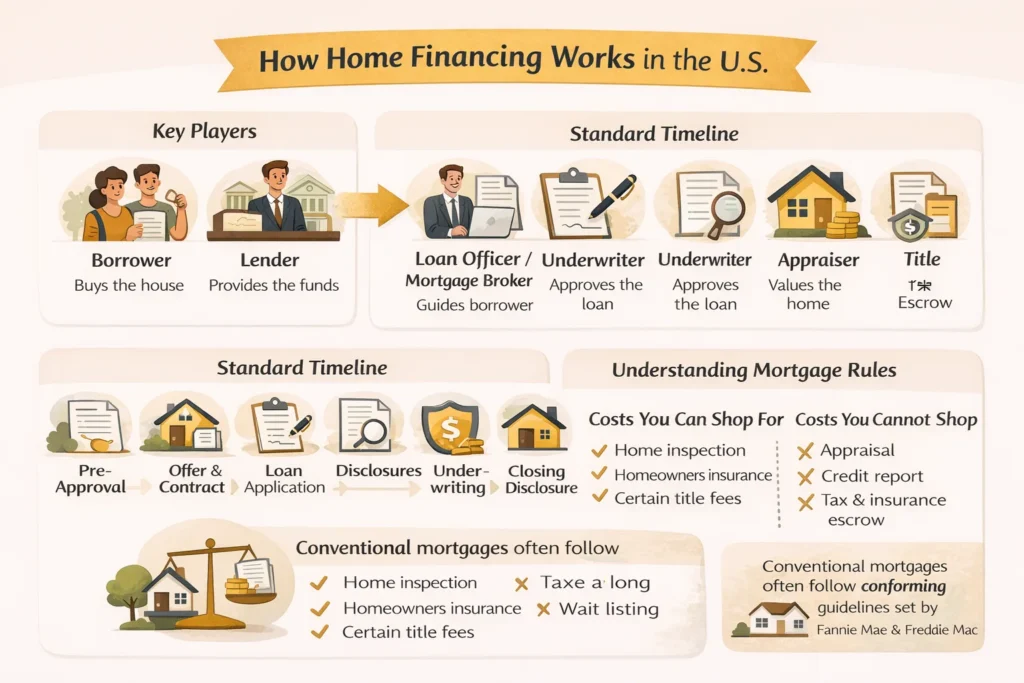

How Home Financing Works in the U.S. (Big Picture)

Home financing in the United States follows a structured process. Federal disclosure laws, underwriting standards, and secondary market rules shape how lenders approve and fund loans. Most buyers follow the same core steps, though timelines and loan types vary.

A typical mortgage takes 30 to 45 days from accepted offer to closing. Cash buyers can close faster, but financed purchases involve document review, property valuation, and legal recording.

Let’s break down the key moving parts.

The players

Several professionals take part in a mortgage transaction. Each has a specific role.

Borrower

The borrower applies for the loan, provides financial documents, and signs the final paperwork. Lenders evaluate the borrower’s credit, income, assets, and debt.

Lender

A lender can be a bank, credit union, or independent mortgage company. The lender funds the loan and sets the qualification standards. Many lenders later sell loans to investors in the secondary market.

Loan officer or mortgage broker

A loan officer works directly for a lender. A mortgage broker works with multiple lenders and helps match borrowers with loan options. Both guide you through the application process.

Underwriter

The underwriter reviews your file in detail. This person verifies income, credit history, employment, assets, and property value. The underwriter decides whether the loan meets lending guidelines.

Appraiser

The appraiser provides an independent opinion of the home’s market value. Lenders require an appraisal to confirm that the property supports the loan amount.

Title and escrow company

The title company checks property records to confirm ownership and identify liens. Escrow professionals manage the exchange of funds and documents. They ensure taxes, insurance, and payoff amounts are handled correctly before the transaction closes.

The standard timeline

The mortgage process follows a clear sequence.

Preapproval

You submit basic financial documents such as pay stubs, tax returns, and bank statements. The lender reviews your credit and issues a preapproval letter. A preapproval strengthens your offer because it shows sellers you meet lending standards.

Offer and contract

You find a home and submit an offer. Once the seller accepts, the contract sets deadlines for inspection, appraisal, and financing.

Loan application and disclosures

The lender issues a Loan Estimate within three business days of receiving your completed application, as required by federal law under the TILA RESPA Integrated Disclosure rules. This document outlines the estimated interest rate, the monthly payment, and the closing costs.

Underwriting

The underwriter reviews the file and may request additional documents. Conditions often include updated bank statements or employment verification.

Appraisal and title review

The appraisal confirms the property value. The title company checks for legal issues tied to the property.

Closing disclosure and closing

The lender provides a Closing Disclosure at least three business days before signing. You review the final loan terms and cash needed at closing. On closing day, you sign documents and ownership transfers to you.

National housing data from the National Association of Realtors consistently shows that financed purchases make up the majority of transactions each year. This structured timeline applies to most homebuyers nationwide.

Why are most mortgages “conforming?”

A large share of U.S. mortgages are called conforming loans. A conforming loan meets guidelines set by Fannie Mae or Freddie Mac. These government-sponsored enterprises buy mortgages from lenders and package them into mortgage-backed securities.

When a loan meets conforming standards, lenders can sell it more easily in the secondary market. That improves liquidity and often results in lower interest rates for borrowers.

Conforming loans must stay under annual loan limits set by the Federal Housing Finance Agency. Loan limits adjust each year based on home price trends. Higher cost areas have higher limits.

Loans that exceed the annual loan limits are called jumbo loans. Jumbo loans typically require stronger credit, larger down payments, and additional documentation because they exceed standard conforming loan limits.

Most first time buyers use conforming loans because they offer competitive rates and predictable guidelines.

What you can shop for and what you can’t

Many buyers assume all mortgage costs are fixed. That is not accurate. Some costs vary by lender, while others depend on third parties.

You can shop for:

- Interest rate

- Lender origination fees

- Discount points

- Certain title and settlement services

- Homeowners insurance

Comparing Loan Estimates from at least two or three lenders helps you see differences clearly. Even a small rate difference can save thousands over the life of a 30-year loan.

You generally cannot shop for:

- Government recording fees

- Transfer taxes set by state or local authorities

- Property tax rates

- Standard appraisal requirements

Federal rules limit how much certain fees can increase between the Loan Estimate and Closing Disclosure. These protections help prevent surprise charges at closing.

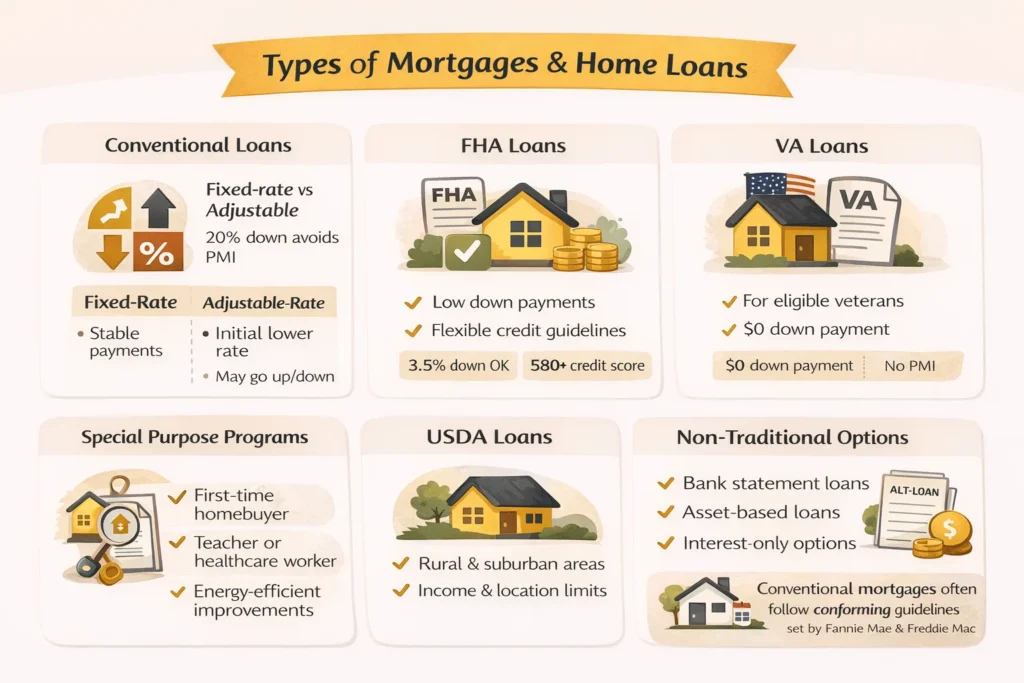

Types of Mortgages and Home Loans

Loan type affects your rate, required down payment, monthly cost, and long-term flexibility. Most borrowers in the United States choose one of a few standard options. Data from federal housing agencies show that conventional and government-backed loans account for the majority of originations each year.

Below is a clear breakdown of each major loan category.

Conventional loans

Conventional loans are not insured by the federal government. Private lenders issue them, and most follow guidelines set by Fannie Mae or Freddie Mac.

Best for:

Buyers with solid credit, stable income, and at least a moderate down payment.

Down payment:

Often as low as 3% for first-time buyers, though 5 to 20% is common.

Mortgage insurance:

Private mortgage insurance, or PMI, applies when the down payment is under 20%. PMI can be removed once you have sufficient equity, per federal law.

Pros:

- Competitive interest rates

- Flexible term options

- Cancelable PMI

- Widely available

Cons:

- Stricter credit standards than some government loans

- Higher rates if the credit score is lower

Conforming vs jumbo

Most conventional loans are conforming loans. That means the loan amount remains below the limits set each year by the Federal Housing Finance Agency. Loan limits adjust annually based on national home price data.

When a loan exceeds the conforming limit for your area, it becomes a jumbo loan.

When jumbo applies:

High-cost housing markets or expensive properties that push loan amounts above annual federal limits.

Jumbo loans usually require:

- Higher credit scores

- Larger down payments

- Stronger cash reserves

Rates on jumbo loans can vary depending on market conditions and investor demand.

Fixed-rate vs adjustable-rate mortgages

The structure of your interest rate changes how your payment behaves over time.

Fixed-rate mortgage

The interest rate stays the same for the entire term.

Best for:

Buyers who plan to stay long term and prefer predictable payments.

Down payment:

Depends on loan type.

Mortgage insurance:

Applies based on loan type and equity level.

Pros:

- Stable monthly payment

- Protection from rising rates

Cons:

- Slightly higher starting rate compared to some ARMs

Adjustable rate mortgage, ARM

The interest rate starts fixed for a set period, then adjusts periodically.

Best for:

Buyers who expect to move or refinance before the adjustment period.

Pros:

- Lower initial interest rate

- Lower starting payment

Cons:

- Payment can increase after a fixed period

ARM structure

A common structure is a 5/1 ARM. The rate stays fixed for five years. After that, it adjusts annually.

Lenders set adjustment caps that limit how much the rate can rise at each change and over the life of the loan. Risk increases if market rates rise sharply after the fixed period. ARMs work best when the borrower has a clear exit plan before adjustments begin.

FHA loans

The Federal Housing Administration insures FHA loans. Private lenders issue them, but the federal government insures them to reduce lenders’ risk.

FHA loans remain popular among first time buyers.

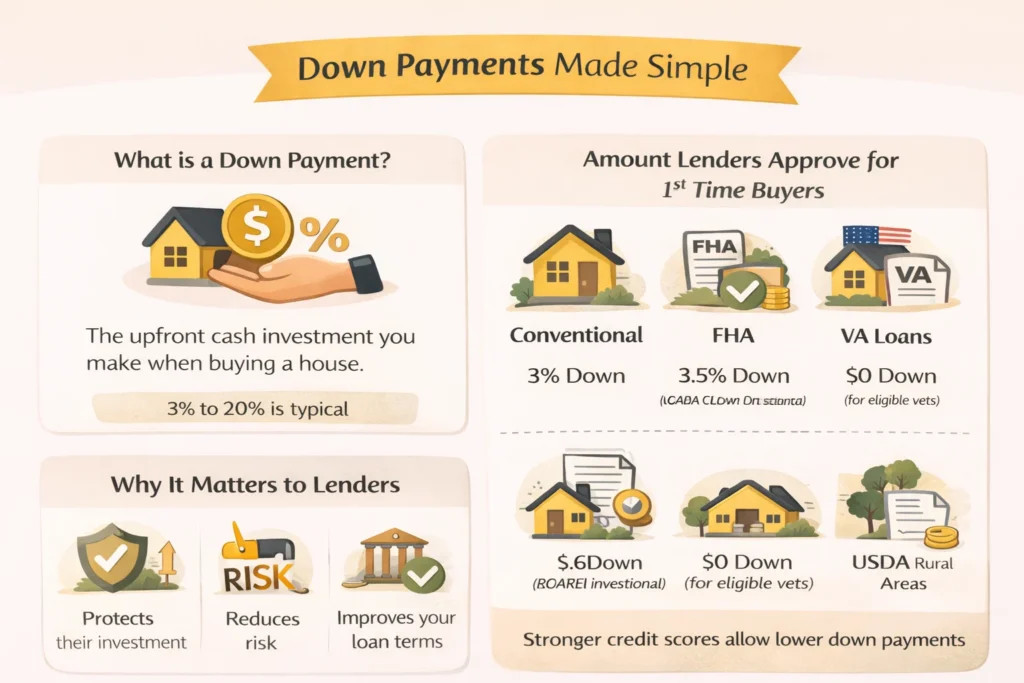

Best for:

Buyers with moderate credit or limited savings.

Down payment:

As low as 3.5% for borrowers who meet minimum credit standards. Lower credit scores may require a higher down payment.

Mortgage insurance:

FHA requires both an upfront mortgage insurance premium and annual insurance included in monthly payments.

Pros:

- More flexible credit requirements

- Lower down payment option

- Competitive rates for certain borrowers

Cons:

- Mortgage insurance may last for the life of the loan in many cases

- Loan limits apply by county

Mortgage insurance basics

Mortgage insurance protects the lender, not the borrower. FHA insurance reduces lender risk when the borrower has a smaller down payment. Insurance increases the total cost of the loan, so long-term planning matters when comparing FHA and conventional options.

VA loans

The Department of Veterans Affairs guarantees VA loans for eligible service members, veterans, and certain surviving spouses.

Best for:

Eligible military borrowers.

Down payment:

Often 0%.

Mortgage insurance:

No monthly mortgage insurance. A one-time funding fee usually applies unless exempt.

Pros:

- No required down payment in many cases

- No ongoing mortgage insurance

- Competitive rates

Cons:

- Eligibility is limited to qualified service members

- Funding fee increases the loan balance if financed

VA loans remain one of the most powerful benefits available to eligible borrowers.

USDA loans

The United States Department of Agriculture backs USDA loans for homes in eligible rural and certain suburban areas.

Best for:

Moderate income buyers purchasing in approved geographic zones.

Down payment:

Often 0%.

Mortgage insurance:

Guarantee fee and annual fee apply.

Pros:

- No required down payment

- Flexible income guidelines

Cons:

- Property must fall within USDA-eligible areas

- Income caps apply

Eligibility maps and income limits are available through USDA program resources.

Special-purpose programs

Several programs exist beyond standard loan categories.

First-time buyer programs and down payment assistance

Many states and local housing agencies offer grants or low-interest second loans to help with down payments and closing costs. Employer-assisted housing programs also exist in some cities.

Program availability depends on income limits, purchase price caps, and residency requirements.

These programs can significantly reduce upfront costs for qualified buyers.

Renovation loans

Renovation loans allow buyers to finance home improvements into the mortgage. Examples include FHA 203 (k)– style programs and certain conventional renovation products.

Non-traditional options

Some loans fall outside standard guidelines.

Interest-only loans

Payments cover interest only for an initial period. Principal payments start later. Risk increases if property values decline or income changes.

Rate buydowns

Temporary or permanent buydowns lower the interest rate early in the loan term. Builders sometimes offer buydowns as incentives.

Non-QM loans

Non-qualified mortgage loans serve borrowers who do not meet traditional income documentation standards. Rates and fees are often higher because lender risk increases.

Down Payments: How Much Do You Actually Need?

A down payment is the portion of the home price you pay upfront. The lender finances the rest. Your down payment directly affects your loan amount, interest cost, and whether you must pay mortgage insurance.

Many buyers believe they need a 20% down payment. That is not true in 2026. The required amount depends on the loan type and your financial profile.

What is a down payment, and why does it matter?

Your down payment reduces the lender’s risk. A larger down payment means you borrow less money and start with more equity in the home.

Example:

A $400,000 home with 5% down requires a $380,000 loan.

The same home with 20% down requires a $320,000 loan.

Smaller loan balances usually mean:

- Lower monthly payments

- Less total interest paid over time

- Better approval odds in competitive markets

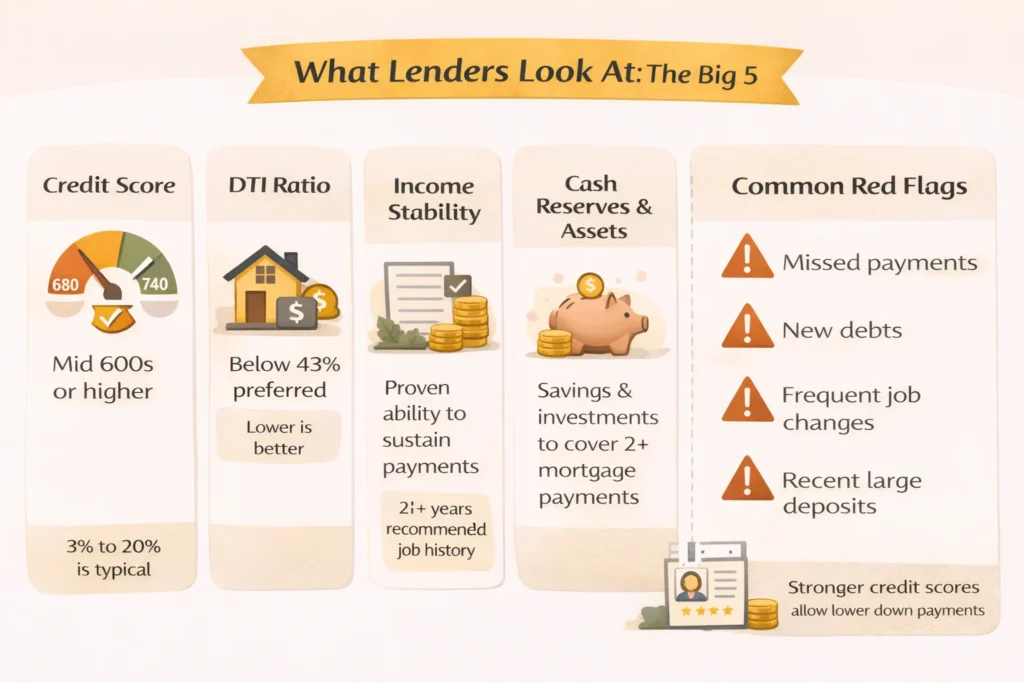

What Lenders Look At: Approval Basics

Mortgage approval follows a risk-based model. Lenders evaluate whether you can repay the loan over time. Underwriters focus on measurable financial factors, not personal opinions.

Federal lending standards and secondary market guidelines shape these reviews. Most lenders follow frameworks tied to Fannie Mae, Freddie Mac, FHA, VA, or USDA rules.

Here are the core factors that matter

Credit score

Your credit score reflects how you have handled debt in the past. It influences three major things:

- Approval likelihood

- Interest rate

- Mortgage insurance cost

Higher scores usually qualify for lower interest rates. Even a small rate difference can affect long-term cost on a 30-year loan.

Many conventional lenders prefer scores in the mid 600s or higher. FHA programs allow lower scores, though pricing and down payment requirements may vary by credit tier.

Late payments, high credit card balances, collections, and recent bankruptcies can lower approval odds. Paying down revolving debt and correcting credit report errors before applying can improve outcomes.

DTI ratio: debt to income

DTI measures how much of your gross monthly income goes toward debt payments.

Lenders calculate it using this formula:

- Total monthly debt payments ÷ Gross monthly income = DTI ratio

Quick example:

You earn 6,000 dollars per month before taxes.

Your total monthly debts, including the new mortgage payment, equal 2,400 dollars.

Your DTI equals 40%.

Many conventional loans prefer DTI ratios below 43%, though approvals may vary based on credit strength and cash reserves. Government-backed loans sometimes allow higher ratios depending on compensating factors.

Lower DTI signals stronger repayment ability.

Income stability

Lenders want predictable income.

W-2 employees usually provide:

- Recent pay stubs

- Two years of W 2 forms

- Tax returns, if required

Self-employed borrowers often provide:

- Two years of personal and business tax returns

- Profit and loss statements

- Business bank statements

Underwriters’ average income over time. Declining income trends raise concerns. Stable or increasing income improves approval odds.

Consistency matters more than a single strong month.

Cash reserves and assets

Lenders review bank statements to confirm you have funds for:

- Down payment

- Closing costs

- Required reserves

Reserves refer to money left after closing. Many lenders prefer to see two to six months of housing payments saved, depending on the loan type and risk profile.

Reserves provide a financial cushion. Strong reserves can offset weaker factors such as higher DTI.

Assets must be properly documented and sourced. Large unexplained deposits often trigger additional review.

Employment history and common red flags

Underwriters look for steady employment over the past two years. Job changes are not automatic problems, but stability helps.

Common red flags include:

- Recent job loss

- Frequent employment gaps

- Sudden shift to commission-based income

- Large unexplained debts

- New credit accounts opened during underwriting

Major financial changes during the loan process can delay or derail approval. Buyers should avoid taking on new loans, making large purchases, or changing jobs until after closing.

If you only remember three things

If you focus on only three approval factors, remember these:

- Maintain strong credit

- Keep your debt-to-income ratio reasonable

- Have enough cash to close and reserves left over

Mortgage approval is not random. It follows structured guidelines. When you understand what lenders evaluate, you can prepare strategically before submitting an application.

Down Payments: How Much Do You Actually Need?

A down payment is the portion of the home price you pay upfront. The lender finances the rest. Your down payment directly affects your loan amount, interest cost, and whether you must pay mortgage insurance.

Many buyers believe they need a 20% down payment. That is not true in 2026. The required amount depends on the loan type and your financial profile.

What is a down payment, and why does it matter?

Your down payment reduces the lender’s risk. A larger down payment means you borrow less money and start with more equity in the home.

Example:

A $400,000 home with 5% down requires a $380,000 loan.

The same home with 20% down requires a $320,000 loan.

Smaller loan balances usually mean:

- Lower monthly payments

- Less total interest paid over time

- Better approval odds in competitive markets

What Lenders Look At: Approval Basics

Mortgage approval follows a risk-based model. Lenders evaluate whether you can repay the loan over time. Underwriters focus on measurable financial factors, not personal opinions.

Federal lending standards and secondary market guidelines shape these reviews. Most lenders follow frameworks tied to Fannie Mae, Freddie Mac, FHA, VA, or USDA rules.

Here are the core factors that matter.

DTI ratio: debt to income

DTI measures how much of your gross monthly income goes toward debt payments.

Lenders calculate it using this formula:

- Total monthly debt payments ÷ Gross monthly income = DTI ratio

Quick example:

You earn 6,000 dollars per month before taxes.

Your total monthly debts, including the new mortgage payment, equal 2,400 dollars.

Your DTI equals 40%.

Many conventional loans prefer DTI ratios below 43%, though approvals may vary based on credit strength and cash reserves. Government-backed loans sometimes allow higher ratios depending on compensating factors.

Lower DTI signals stronger repayment ability.

Income stability

Lenders want predictable income.

W-2 employees usually provide:

- Recent pay stubs

- Two years of W 2 forms

- Tax returns, if required

Self-employed borrowers often provide:

- Two years of personal and business tax returns

- Profit and loss statements

- Business bank statements

Underwriters’ average income over time. Declining income trends raise concerns. Stable or increasing income improves approval odds.

Consistency matters more than a single strong month.

Cash reserves and assets

Lenders review bank statements to confirm you have funds for:

- Down payment

- Closing costs

- Required reserves

Reserves refer to money left after closing. Many lenders prefer to see two to six months of housing payments saved, depending on the loan type and risk profile.

Reserves provide a financial cushion. Strong reserves can offset weaker factors such as higher DTI.

Assets must be properly documented and sourced. Large unexplained deposits often trigger additional review.

Employment history and common red flags

Underwriters look for steady employment over the past two years. Job changes are not automatic problems, but stability helps.

Common red flags include:

- Recent job loss

- Frequent employment gaps

- Sudden shift to commission-based income

- Large unexplained debts

- New credit accounts opened during underwriting

Major financial changes during the loan process can delay or derail approval. Buyers should avoid taking on new loans, making large purchases, or changing jobs until after closing.

If you only remember three things

If you focus on only three approval factors, remember these:

- Maintain strong credit

- Keep your debt-to-income ratio reasonable

- Have enough cash to close and reserves left over

Mortgage approval is not random. It follows structured guidelines. When you understand what lenders evaluate, you can prepare strategically before submitting an application.

Mortgage Rates Explained and How to Get a Better One

Your mortgage rate determines how much interest you pay over the life of the loan. Even a small difference can change your total cost by thousands of dollars on a 30-year term.

Rates move daily based on bond markets, inflation data, and Federal Reserve policy. Lenders then adjust pricing based on your personal risk profile.

Here is what shapes your rate and how you can influence it.

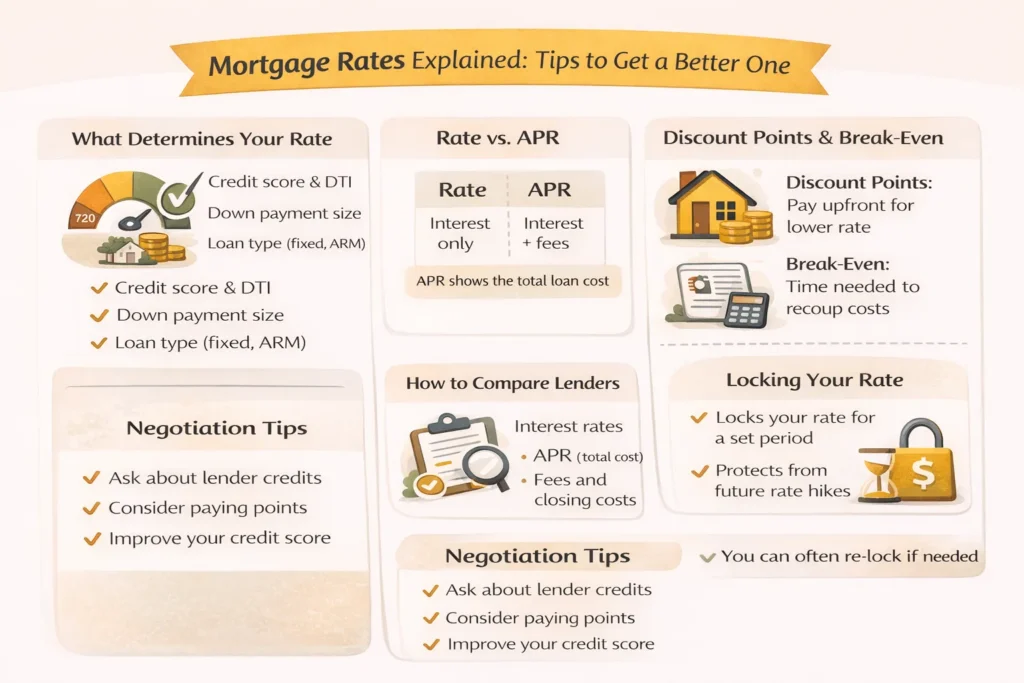

What determines your rate

Lenders price mortgages based on measurable risk factors.

Credit score

Higher scores usually qualify for lower rates. Strong credit signals lower default risk.

Down payment

Larger down payments reduce lender risk. That often results in better pricing.

Loan type

Conventional, FHA, VA, and jumbo loans carry different pricing structures. Government-backed loans may offer competitive rates for certain borrowers.

Loan term

Shorter terms, such as 15 years, often carry lower interest rates than 30-year loans. Monthly payments are higher because the payoff period is shorter.

Discount points

Borrowers can pay upfront fees to reduce the interest rate.

Market conditions also matter. Mortgage rates typically follow movements in the 10-year Treasury yield, though they are not identical.

Rate vs APR

The interest rate shows the cost of borrowing the principal.

APR, or annual percentage rate, reflects the broader cost of the loan. It includes the interest rate plus certain lender fees expressed as a yearly percentage.

Federal law requires lenders to disclose APR under the Truth in Lending Act. APR gives you a more complete comparison tool when reviewing Loan Estimates.

Example:

Loan A offers a 6.50% rate with higher fees.

Loan B offers a 6.75% rate with lower fees.

- APR may reveal that Loan B costs less over time despite the slightly higher rate.

- APR becomes especially useful when comparing offers with different fee structures.

Discount points and the breakeven concept

One discount point usually equals 1% of the loan amount. Paying points reduces your interest rate.

Example:

On a 400,000 dollar loan, one point costs 4,000 dollars.

If paying that point lowers your rate and saves 100 dollars per month, your breakeven point is 40 months.

Breakeven formula:

- Cost of points ÷ Monthly savings = Months to recover cost

Points make sense if you plan to keep the loan longer than the breakeven period. They make less sense if you expect to sell or refinance soon.

How to compare lenders

Serious buyers should request Loan Estimates from at least two or three lenders.

Federal rules require lenders to provide a Loan Estimate within 3 business days of receiving a completed application. This document shows:

- Interest rate

- Estimated monthly payment

- Closing costs

- APR

Compare lenders using the same loan term and rate structure. Focus on total cost, not just the advertised rate.

Small rate differences can significantly affect the lifetime interest on long-term loans.

Locking your rate

A rate lock guarantees your quoted interest rate for a specific period, often 30 to 60 days.

Rates can rise or fall before closing. Locking protects you from market increases during the loan process.

Timing matters. Lock too early, and you may pay extension fees if closing gets delayed. Locking too late could increase rates.

Loan officers monitor market conditions and expected closing dates to recommend appropriate lock periods.

Mortgage rates influence affordability more than most buyers realize. Preparing your credit, comparing lenders, and understanding pricing tools can reduce long-term borrowing costs.

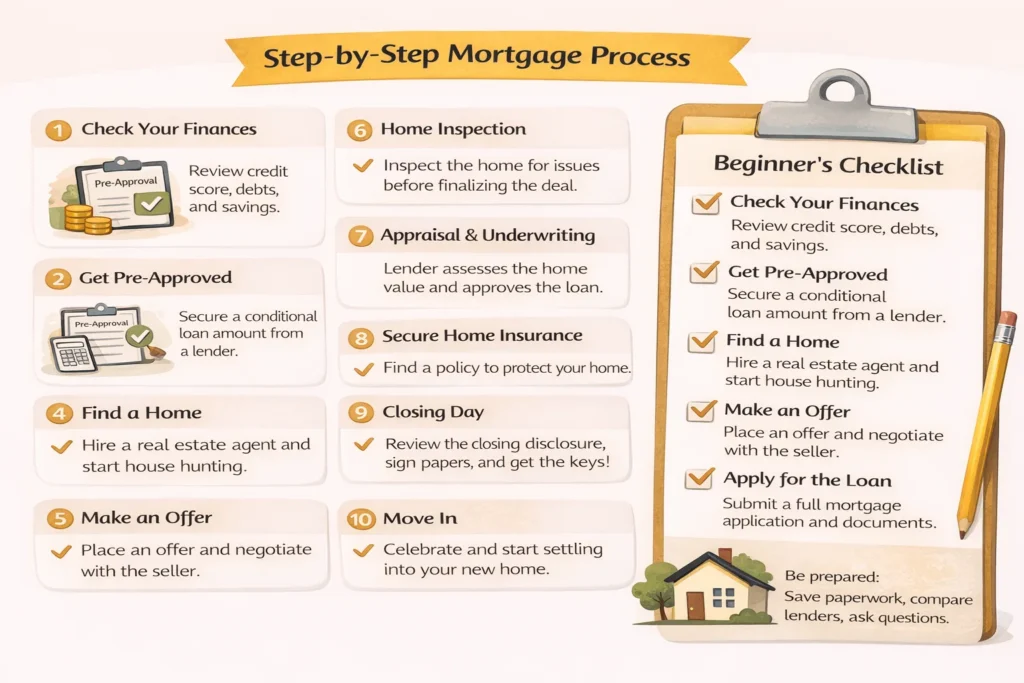

The Step-By-Step Mortgage Process: Beginner Checklist

Most financed home purchases in the United States follow a similar path. The full process usually takes 30 to 45 days after your offer is accepted. Preparation reduces stress and prevents delays.

Here is a clear checklist from start to finish.

Step 1 — Set a realistic budget

Start with the full housing cost, not just the loan payment.

Your monthly housing expense usually includes:

- Principal

- Interest

- Property taxes

- Homeowners insurance

Many lenders refer to this as PITI.

You should also account for:

- Utilities

- HOA dues, if applicable

- Maintenance and repairs

Financial planners often recommend budgeting 1-3% of a home’s value annually for maintenance. That protects you from unexpected repair costs.

A strong budget keeps your debt-to-income ratio within approval limits and reduces long-term stress.

Step 2 — Prequalified vs preapproved

Prequalification is an informal estimate. It often relies on self-reported information and a soft credit check.

Preapproval involves document review and a hard credit pull. The lender verifies income, assets, and credit before issuing a letter.

Preapproval carries more weight with sellers. In competitive markets, many listing agents require a preapproval letter before accepting an offer.

Serious buyers should pursue preapproval before aggressively house hunting.

Step 3 — Choose a lender or mortgage broker

Compare lenders based on:

- Interest rate and APR

- Total lender fees

- Responsiveness and communication

- Experience with your loan type

Request Loan Estimates from multiple lenders using similar loan terms. Clear communication is essential because delays often result from missing documents or slow responses.

A strong loan officer guides you through underwriting and keeps the process moving.

Step 4 — Gather documents

Most lenders request:

- Government-issued ID

- Recent pay stubs

- Two years of W-2 forms or tax returns

- Bank statements

- Documentation for large deposits

- Information about current debts

Self-employed borrowers may need additional business documentation.

Providing complete and organized documents reduces underwriting delays.

Step 5 — Make an offer and include contingencies

Once you find a property, your real estate agent submits an offer. The contract often includes contingencies that protect you.

Common contingencies include:

- Inspection contingency

- Financing contingency

- Appraisal contingency

These conditions allow you to withdraw or renegotiate if serious issues arise.

A financing contingency protects your earnest money if the loan is denied under the contract terms.

Step 6 — Underwriting

Underwriting is the formal risk review.

The underwriter:

- Verifies income and employment

- Confirms asset documentation

- Reviews credit history

- Evaluates the appraisal

Conditional approval is common. The lender may request updated statements or clarification letters. Quick responses help keep closing on schedule.

Avoid opening new credit accounts or changing jobs during this stage.

Step 7 — Appraisal and inspection

The appraisal determines whether the property value supports the loan amount.

The inspection assesses the home’s condition. Inspectors look for structural issues, safety concerns, and major system problems.

Appraisal protects the lender. Inspection protects you.

If the appraisal comes in low, renegotiation may be required. If inspection reveals serious defects, you can request repairs or credits.

Step 8 — Closing day

At least three business days before closing, the lender provides a Closing Disclosure. This document lists final loan terms and the exact cash required.

On closing day, you sign:

- The promissory note

- The mortgage or deed of trust

- Title documents

You pay your down payment, closing costs, and prepaid items such as insurance and property taxes.

Once documents are recorded with the county, ownership transfers to you.

Step 9 — First 90 days as a homeowner

Your first mortgage payment usually comes due one month after closing.

If your loan includes escrow, the lender collects monthly funds for property taxes and insurance. Monitor your escrow statements to ensure accuracy.

Many states offer homestead exemptions that reduce property tax liability for primary residences. Check with your local tax authority to apply if eligible.

Keep copies of all closing documents in a secure location. You may need them for tax reporting and future refinancing.

Following this checklist keeps your purchase organized and predictable. Each step builds on the previous one, and preparation remains your strongest advantage.

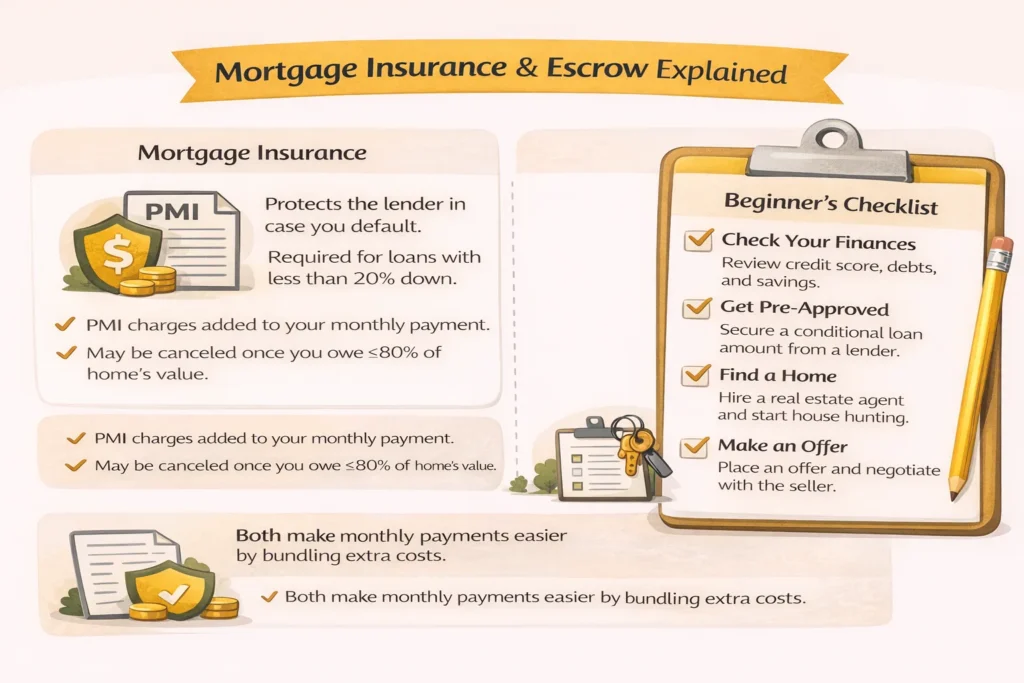

Mortgage Insurance and Escrow: Plain English Explanation

Many first-time buyers feel confused when they see extra charges added to their monthly payment. Two of the most common are mortgage insurance and escrow.

These costs protect the lender and keep the required bills current. They do not build equity in your home, but they are part of many mortgage structures.

PMI vs FHA mortgage insurance

Mortgage insurance protects the lender if a borrower defaults. It applies when the down payment is small.

PMI on conventional loans

Private mortgage insurance applies when you put down less than 20% on a conventional loan.

- Paid monthly as part of your mortgage payment

- Cost depends on credit score and down payment size

- Can usually be removed once you reach enough equity

Stronger credit and larger down payments reduce PMI cost.

FHA mortgage insurance

FHA loans require two types of insurance:

- An upfront mortgage insurance premium

- An annual premium paid monthly

In many FHA cases, the annual premium lasts for the life of the loan if the down payment is under 10%. That makes long-term cost comparisons important when choosing between FHA and conventional options.

Both PMI and FHA insurance lower lender risk. That risk reduction allows buyers to qualify with smaller down payments.

What escrow is

Escrow is a separate account your lender uses to collect property taxes and homeowners’ insurance premiums.

Each month, a portion of your payment is placed in escrow. The lender then pays your tax bill and insurance premium when they come due.

Escrow protects:

- The lender, because unpaid taxes can create liens

- You, because the required bills get paid on time

Lenders often require escrow when the down payment is under 20%. Some lenders allow escrow waivers for borrowers with higher equity, though fees may apply.

Your lender performs an annual escrow analysis to adjust for tax or insurance changes. That review can increase or decrease your monthly payment.

When you can remove PMI

Federal law under the Homeowners Protection Act provides borrowers with certain rights regarding the removal of PMI on conventional loans.

In general:

- You can request removal once your loan balance reaches 80% of the home’s original value.

- Lenders must automatically terminate PMI when the balance reaches 78%, assuming payments are current.

You may need to provide an appraisal if property values have changed significantly.

FHA mortgage insurance follows different rules. Removal often requires refinancing into a conventional loan if equity and credit qualify.

Understanding when and how insurance ends can save thousands over time. A separate detailed guide can walk through the full PMI removal process step by step.

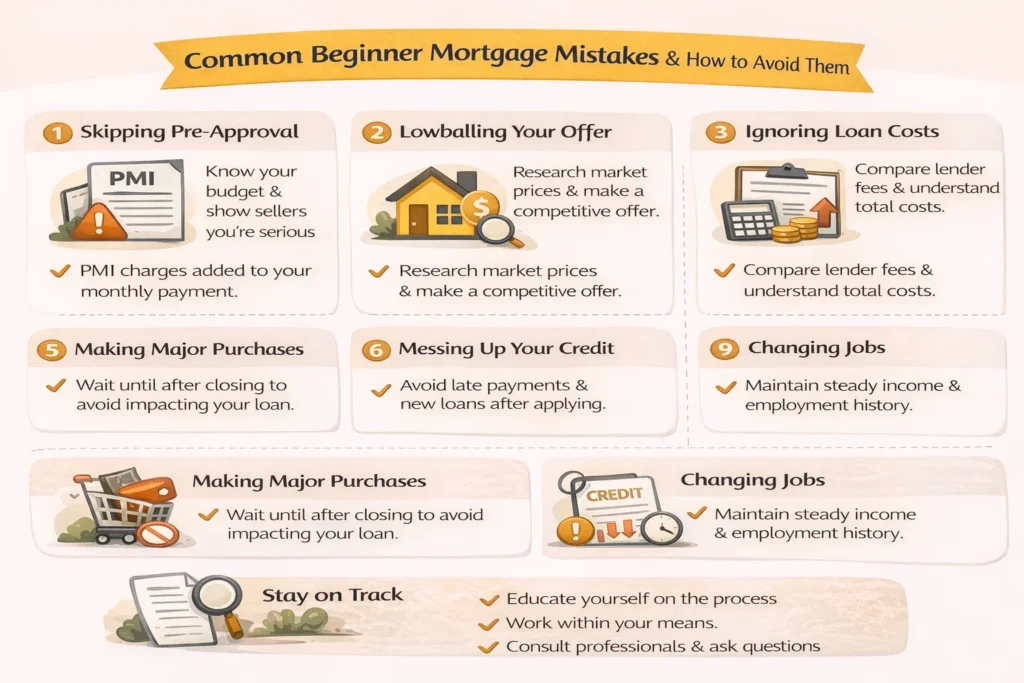

Common Beginner Mistakes and How to Avoid Them

Mortgage approvals follow strict guidelines. Small financial changes can create major delays. Many first-time buyers encounter preventable issues during the process.

Here are the most common mistakes and how to avoid them.

Changing jobs or opening new credit during underwriting

Underwriting relies on stable income and consistent credit.

A new job can delay approval because the lender must re-verify employment and income. A switch from salaried to commission-based pay creates even more scrutiny.

Opening new credit accounts also increases risk. A new car loan or credit card changes your debt-to-income ratio and can lower your credit score.

Keep your financial profile steady until after closing. Avoid large purchases, new loans, or employment changes during the loan process.

Spending your down payment savings before closing

Lenders review updated bank statements before final approval. Large withdrawals can raise concerns about available funds.

Your cash to close includes:

- Down payment

- Closing costs

- Prepaid taxes and insurance

If funds drop below required levels, the lender may delay or deny final approval.

Protect your savings until the transaction is complete. Wait to buy furniture or appliances after you receive the keys.

Skipping inspection contingencies

In competitive markets, some buyers waive inspection contingencies to strengthen their offer. That decision carries risk.

Home inspections can uncover:

- Structural issues

- Roof damage

- Plumbing or electrical problems

- Safety hazards

Repair costs can easily reach thousands of dollars. Inspection contingencies give you leverage to renegotiate or withdraw if serious defects appear.

Removing that protection makes sense only after careful consideration and professional guidance.

Shopping only by monthly payment

Some buyers focus only on the quoted monthly payment. That approach can hide long-term cost differences.

A lower payment today might result from:

- Adjustable rates

- Longer loan terms

- Higher upfront fees

- Mortgage insurance

APR provides a clearer comparison tool because it reflects the broader cost of borrowing. Comparing Loan Estimates side by side helps reveal fee differences that affect total cost.

Smart borrowers evaluate the full financial picture, not just the initial payment.

Avoiding these mistakes keeps your purchase on track and protects your long-term financial stability.

Can Settlement Funds Help You Buy a Home?

Buying a home requires upfront capital. Many lenders require funds for a down payment, closing costs, and cash reserves.

If you sell structured settlement payments, annuity income, or lottery installments, your income may be spread out over time. That structure can make it harder to quickly accumulate a large lump sum.

In some cases, selling a portion of future payments may provide immediate liquidity. A lump sum could potentially be used toward:

- Down payment

- Paying off high-interest debt

- Building cash reserves required by lenders

Structured settlement transfers require court approval and should be evaluated carefully. Long-term financial impact matters.

Citrine Capital works with individuals nationwide who are considering structured settlement buyouts, annuity sales, lottery payment transfers, or pre-settlement funding.

If you are planning a home purchase and exploring ways to improve your financial position, reviewing your settlement options may be worth discussing with a financial professional.

Frequently Asked Questions

Below are clear, direct answers designed to address common search queries about home loans and mortgages in the United States.

What credit score do I need to qualify for a mortgage?

Most conventional lenders look for a credit score in the mid 600s or higher. FHA loans may accept lower scores, though interest rates and down payment requirements can vary by credit tier.

Higher scores improve approval odds and usually qualify for better interest rates and lower mortgage insurance costs.

How much of a down payment do first-time buyers need?

Many first-time buyers qualify for as little as 3% down on certain conventional programs. FHA loans require 3.5% for borrowers who meet minimum credit standards. VA and USDA loans may allow zero down for eligible buyers.

The required amount depends on loan type, credit profile, and property location.

What is the difference between preapproval and prequalification?

Prequalification is an informal estimate based on self-reported financial information.

Preapproval involves document review and a credit check. The lender verifies income, assets, and credit before issuing a letter.

Sellers view preapproval as stronger proof of financing.

How much are closing costs in the United States?

Closing costs typically range from 2% to 5% of the home price. The total depends on loan type, lender fees, property taxes, and local recording charges.

Your Loan Estimate outlines expected closing costs early in the process.

What is a Loan Estimate, and when do I get it?

A Loan Estimate is a standardized form that outlines your interest rate, estimated monthly payment, and closing costs.

Federal law requires lenders to provide it within three business days after you submit a completed mortgage application.

It helps you compare loan offers clearly.

What is a Closing Disclosure, and when do I get it?

A Closing Disclosure lists your final loan terms and the exact cash required at closing.

Lenders must provide it at least three business days before you sign the closing documents. This waiting period gives you time to review final costs.

What is escrow, and why do lenders use it?

Escrow is an account your lender uses to collect property taxes and homeowners’ insurance premiums. You pay a portion each month as part of your mortgage payment.

Lenders use escrow to ensure taxes and insurance remain current, which protects the property securing the loan.

FHA vs conventional: which is better for me?

FHA loans often work well for buyers with moderate credit or smaller down payments. Conventional loans may cost less over time if you have stronger credit and can remove private mortgage insurance once you build equity.

The better option depends on your credit score, down payment size, and long term plans.

Fixed rate vs ARM: which one should a beginner choose?

A fixed-rate mortgage offers stable payments for the entire loan term. It works well for buyers planning to stay long term.

An adjustable-rate mortgage starts with a lower rate that adjusts after a set period. It may suit buyers who expect to move or refinance before the adjustment period begins.

Risk tolerance and time horizon should guide this decision.

Can I buy a house with student loan debt?

Yes. Lenders include student loan payments in your debt-to-income ratio. Approval depends on how that debt affects your overall DTI and credit profile.

Lower DTI and consistent payment history improve approval chances.

How long does it take to close on a mortgage?

Most financed purchases close within 30 to 45 days after contract acceptance. The timeline depends on appraisal scheduling, underwriting conditions, and document response times.

Preparation helps prevent delays.

Can I pay off my mortgage early?

Most standard mortgages do not include prepayment penalties. You can make extra principal payments or refinance if beneficial.

Always review your loan documents to confirm terms.

Do I need 20% down to avoid problems?

No. Many buyers purchase homes with less than 20% down. A larger down payment reduces loan size and may eliminate private mortgage insurance, but it is not required for approval in many programs.

What happens if the appraisal comes in low?

If the appraised value is lower than the purchase price, you can renegotiate with the seller, increase your down payment, or cancel the contract if an appraisal contingency exists.

Appraisal protects the lender from over-lending.

Can mortgage rates change after I get preapproved?

Yes. Preapproval does not lock your rate. Rates can change daily until you lock them with your lender.

A rate lock protects you from market increases during the agreed lock period.